BCOE 143 Solved Assignment 2022 – 23

IGNOU BCOMG – 5TH Semester

COURSE CODE: BCOE 143 Fundamentals of Financial Management

TUTOR MARKED ASSIGNMENT B. COMG 5th SEM

ASSIGNMENT CODE: BCOC-132/TMA/2022-23

Maximum Marks: 100

SECTION-A

(This section contains long answer questions of 10 marks each)

In this post you will get BCOE 143 Solved Assignment 2022 – 23. Subject Title is Fundamentals of Financial Management which is an important subject of IGNOU BCOMG 5th Semester. All the IGNOU BCOMG solved assignment are free. Visit our blog regularly for more solved assignment.

1. Discuss capital asset pricing model. (10)

Ans: Capital Asset Pricing Model (CAPM)

Capital market theory is an extension of the Portfolio theory of Markowitz. The portfolio theory explains how rational investors should build efficient portfolio based on their risk-return preferences. Capital Market Asset Pricing Model (CAPM) incorporates a relationship, explaining how assets should be prices in the capital market. The capital market theory uses the results of capital market theory to derive the relationship between the expected returns and systematic risk of individual securities and portfolios.

Capital asset pricing model is a tool used by investors to determine the risk associated with a potential investment and also gives an idea as to what can be the expected return on the investment. It was developed by William Sharpe along with a formula for working out the risk as who states that with an investment come two types of risks:

1) Systematic Risk: These are risks that cannot be diversified away such as interest rates and recessions. As the market moves and changes occur which affect the market, each individual asset is affected to some degree and therefore they are sensitive to change causing a high level of risk.

2) Unsystematic (Specific): These risk can be diversified through increasing the size of an investment portfolio as this risk is specific to individual stocks and effectively represents no correlation between stocks and market movements.

CAPM states that investors are compensated for taking systematic risk however not for taking specific risk as an investor can diversify this risk away. Systematic risk cannot be eliminated of course even by holding all the shares in a stock market; therefore, CAPM has introduced a method of calculating that risk.

Mathematical expression of CAPM: It can be expressed mathematically with the help of following equation:

E (rA) = rf + βA (E (rM) – rf)

where:

E (rA) is the expected return of the asset

rf is the risk-free rate

E (rM) is the expected return of the market portfolio

The general idea of CAPM is that investors should be compensated in two ways: time value of money and risk.The time value of money is represented by the risk-free (rf) rate in the formula and compensates the investors for placing money in any investment over a period of time.The other part of the formula represents risk and calculates the amount of compensation the investor needs for taking on additional risk. This is done by taking an estimate of risk, (βA), and multiplying by the MRP, (E (rM) – rf).

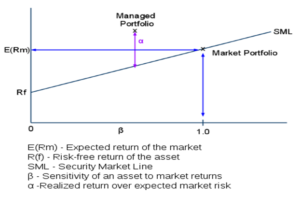

Graphical Presentation of CAMP

An asset is expected to earn the risk-free rate plus a reward for bearing risk as measured by that asset’s beta. The chart below demonstrates this predicted relationship between beta and expected return – this line is called the Security Market Line.

For example, a stock with a beta of 1.5 would be expected to have an excess return of 15% in a time period where the overall market beat the risk-free asset by 10%. The CAPM model is used for pricing an individual security or a portfolio. For individual securities, the security market line (SML) and its relation to expected return and systematic risk (beta) shows how the market must price individual securities in relation to their security risk class.

As the CAPM predicts expected returns of assets or portfolios relative to risk and market return, the CAPM can also be used to evaluate the performance of active fund managers. The difference is “excess return”, which is often referred to as alpha (α). If α is greater than zero, the portfolio lies above the Security Market Line.

2. A bond of Rs. 5,000 is redeemable after 10 years. The coupon rate of the bond is 12%. Find out the value of the bond if the required rate of return is 12%. The maturity of the bond is (a) 8 years (b) 10 years. (10)

Ans: Coming Soon

3. Explain briefly the long term sources of finance. (10)

Ans: Sources of Long Term Finance:

– Equity Shares

– Preference Shares

– Retained Shares

– Debentures

– Bonds

– Term loans

– Loan from Financial institutions

a) Equity shares: Equity shares are instruments to raise equity capital. The equity share capital is the backbone of any company’s financial structure. Equity capital represents ownership capital. Equity shareholders collectively own the company. They enjoy the reward of ownership and bear the risk of ownership. The equity share capital is also termed as the venture capital on account of the risk involved in it. The equity shareholders’ liability, unlike the liability of the owner in a proprietary concern and the partners in a partnership concern, is limited to their capital contribution.

b) Preference Shares: According to Sec. 43 (a) of the Companies Act 2013, a share that carries the following two preferential rights is called ‘Preference Share’:

(i) Preference shares have a right to receive dividend at a fixed rate before any dividend given to equity Shares.

(ii) Preference shares have a right to get their capital returned, before the capital of equity shareholders is returned in case the company is going to wind up.

In case of preference shares, the rate of dividend is fixed and the dividend on these shares must be paid before any dividend is paid to equity shareholders. Directors, however, may decide not to pay any dividend to any class of shareholders even if there are sufficient profits.

c) Retained Earnings: Retained earnings are internal sources of finance for any company. Actually is not a method of raising finance, but it is called as accumulation of profits by a company for its expansion and diversification activities. Retained earnings are called under different names such as self-finance; inter finance, and plugging back of profits. As prescribed by the central government, a part (not exceeding 10%) of the net profits after tax of a financial year have to be compulsorily transferred to reserve by a company before declaring dividends for the year.

d) Debentures: Debentures are debt securities issued by a joint stock company. Amounts collected by way of debentures form part of the loan capital of a company and are repayable after a fixed period. Debenture holders get fixed rate of interest on their debentures as a charge against profit. They are creditors of the company.

e) Bonds: Bonds, like debentures, is an acknowledgement of debt issued under the common seal of a company. The only difference between bonds and debentures is that rate of interest is not pre-determined in case of bond, but in case of debentures rate of interest is fixed.

f) Term Loans: A loan which is financed by the banks and financial institutions for medium term upon the primary security of assets and collateral security of other assets is known as term loan. This type of loan is primarily used for expansion of business that is why it is also called project financing. A fixed rate of interest is charged on term loans and it is always payable in installments.

g) Loan from Financial institutions: Long term loans can also be raised from financial institutions such as LICI, IDBI, IFCI and other development banks.

4. The cost of a project is Rs. 30,00,000 and its life is 5 years. The cash flows are given below: (10)

|

Years |

Cash flows |

|

1 |

4,00,000 |

|

2 |

6,00,000 |

|

3 |

6,00,000 |

|

4 |

10,00,000 |

|

5 |

8,00,000 |

The cost of capital is 10%. Find out the net present value of the project.

Ans: Coming Soon

5. Explain the Walter’s Valuation Model. (10)

Ans: Walter’s Dividend theory

Professor James E. Walter argues that the choice of dividend policies almost always affects the value of the enterprise. His model shows clearly the importance of the relationship between the firm’s internal rate of return (r) and its cost of capital (k) in determining the dividend policy that will maximise the wealth of shareholders.

Valuation Formula and its Denotations: Walter’s formula to calculate the market price per share (P) is:

P = D/k + {r*(E-D)/k}/k, where

P = market price per share

D = dividend per share

E = earnings per share

r = internal rate of return of the firm

k = cost of capital of the firm

Explanation: The mathematical equation indicates that the market price of the company’s share is the total of the present values of:

a) An infinite flow of dividends, and

b) An infinite flow of gains on investments from retained earnings.

The formula can be used to calculate the price of the share if the values of other variables are available.

Walter’s model is based on the following assumptions:

a) The firm finances all investment through retained earnings; that is debt or new equity is not issued;

b) The firm’s internal rate of return (r), and its cost of capital (k) are constant;

c) All earnings are either distributed as dividend or reinvested internally immediately.

d) Beginning earnings and dividends never change. The values of the earnings per share (E), and the divided per share (D) may be changed in the model to determine results, but any given values of E and D are assumed to remain constant forever in determining a given value.

e) The firm has a very long or infinite life.

Criticism of Walter’s theory:

Walter’s model is quite useful to show the effects of dividend policy on an all equity firm under different assumptions about the rate of return. However, the simplified nature of the model can lead to conclusions which are net true in general, though true for Walter’s model.The criticisms on the model are as follows:

1. Walter’s model of share valuation mixes dividend policy with investment policy of the firm. The model assumes that the investment opportunities of the firm are financed by retained earnings only and no external financing debt or equity is used for the purpose when such a situation exists either the firm’s investment or its dividend policy or both will be sub-optimum. The wealth of the owners will maximise only when this optimum investment in made.

2. Walter’s model is based on the assumption that r is constant. In fact, decreases as more investment occurs. This reflects the assumption that the most profitable investments are made first and then the poorer investments are made.The firm should step at a point where r = k. This is clearly an erroneous policy and fall to optimize the wealth of the owners.

3. A firm’s cost of capital or discount rate, K, does not remain constant; it changes directly with the firm’s risk. Thus, the present value of the firm’s income moves inversely with the cost of capital. By assuming that the discount rate, K is constant, Walter’s model abstracts from the effect of risk on the value of the firm.

Section – B

6. Explain the factors affecting cost of capital. (6)

Ans: Buy Full Solved Assignment @ Rs. 30

7. From the following data calculate degree of operating leverage of the firm ‘A’ (6)

|

Particulars |

Firm ‘A’ |

|

Sales |

Rs. 40,00,000 |

|

Variable Cost |

20% Sales |

|

Fixed Cost |

Rs. 10,00,000 |

Ans: Coming soon

8. Discuss M & M model of capital structure without taxes. (6)

Ans: Modigliani and Miller Approach (MM Approach): According to this approach, the total cost of capital of particular firm is independent of its method and level of financing. Modigliani and Miller argued that the weighted average cost of capital of a firm is completely independent of its capital structure.

In other words, a change in the debt equity mix does not affect the cost of capital. They argued, in support of their approach, that as per the traditional approach, cost of capital is the weighted average of cost of debt and cost of equity, etc. The cost of equity, is determined from the level of shareholder’s expectations. That is if, shareholders expect a particular rate of return, say 15 % from a particular company, they do not take into account the debt equity ratio and they expect 15 % as they find that it covers the particular risk which this company entails.

Thus, the shareholders would now, expect a higher rate of return from the shares of the company. Thus, each change in the debt equity mix is automatically set-off by a change in the expectations of the shareholders from the equity share capital. Modigliani and Miller, thus, argue that financial leverage has nothing to do with the overall cost of capital and the overall cost of capital is equal to the capitalisation rate of pure equity stream of its class of risk. Thus, financial leverage has no impact on share market prices nor on the cost of capital.

Assumptions:

i) The capital markets are assumed to be perfect. This means that investors are free to buy and sell securities.

a) They are well-informed about the risk-return on all type of securities.

b) There are no transaction costs.

c) They behave rationally.

d) They can borrow without restrictions on the same terms as the firms do.

ii) The firms can be classified into ‘homogenous risk class’. They belong to this class, if their expected earnings have identical risk characteristics.

iii) All investors have the same expectations from a firms’ EBIT that is necessary to evaluate the value of a firm.

iv) The dividend payment ratio is 100 %. i.e. there are no retained earnings.

v) There are no corporate taxes, but, this assumption has been removed.

Modigliani and Miller agree that while companies in different industries face different risks resulting in their earnings being capitalised at different rates, it is not possible for these companies to affect their market values, and thus, their overall capitalisation rate by use of leverage. That is, for a company in a particular risk class, the total market value must be same irrespective of proportion of debt in company’s capital structure. The support for this hypothesis lies in the presence of arbitrage in the capital market. They contend that arbitrage will substitute personal leverage for corporate leverage.

9. Explain the assumptions and limitations of Gordon model. (6)

Ans: Assumptions of Gordon’s Model:

1) The firm is an all-equity firm; only the retained earnings are used to finance the investments, no external source of financing is used.

2) The rate of return (r) and cost of capital (K) are constant.

3) The life of a firm is indefinite.

4) Retention ratio once decided remains constant.

5) Growth rate is constant (g = br).

6) Cost of Capital is greater than br.

Criticism of Gordon’s Model

1) It is assumed that firm’s investment opportunities are financed only through the retained earnings and no external financing viz. Debt or equity is raised. Thus, the investment policy or the dividend policy or both can be sub-optimal.

2) The Gordon’s Model is only applicable to all equity firms. It is assumed that the rate of returns is constant, but, however, it decreases with more and more investments.

3) It is assumed that the cost of capital (K) remains constant but, however, it is not realistic in the real life situations, as it ignores the business risk, which has a direct impact on the firm’s value.

10. What is an operating cycle? Why is it important for the firm? (6)

Ans: Ans: Buy Full Solved Assignment @ Rs. 30

Section – C

11. What is financial leverage? How is it measured? (5)

Ans: A Leverage activity with financing activities is called financial leverage. Financial leverage represents the relationship between the company’s earnings before interest and taxes (EBIT) or operating profit and the earning available to equity shareholders. Financial leverage is defined as “the ability of a firm to use fixed financial charges to magnify the effects of changes in EBIT on the earnings per share”. It involves the use of funds obtained at a fixed cost in the hope of increasing the return to the shareholders. Financial leverage can be calculated with the help of the following formula:

FL = OP/PBT

Where,

FL = Financial leverage

OP = Operating profit (EBIT)

PBT = Profit before tax.

Degree of Financial Leverage: Degree of financial leverage may be defined as the percentage change in taxable profit as a result of percentage change in earnings before interest and tax (EBIT). This can be calculated by the following formula: DFL= Percentage change in taxable Income / Percentage change in EBIT

12. Explain Baumol’s model of cash management. (5)

Ans: Buy Full Solved Assignment @ Rs. 30

13. Explain ‘Credit standard’ and ‘credit period’. (5)

Ans: Buy Full Solved Assignment @ Rs. 30

14. What is ABC analysis? (5)

Ans: ABC Analysis:In this technique, the items of inventory are classified according to the value of usage. Materials are classified as A, B and C according to their value.

Items in class ‘A’ constitute the most important class of inventories so far as the proportion in the total value of inventory is concerned. The ‘A’ items constitute roughly about 5-10% of the total items while its value may be about 80% of the total value of the inventory.

Items in class ‘B’ constitute intermediate position. These items may be about 20-25% of the total items while the usage value may be about 15% of the total value.

Items in class ‘C’ are the most negligible in value, about 65-75% of the total quantity but the value may be about 5% of the total usage value of the inventory.

The numbers given above are just indicative, actual numbers may vary from situation to situation. The principle to be followed is that the high value items should be controlled more carefully while items having small value though large in numbers can be controlled periodically.

Advantages of ABC analysis

a. Reduction in investment: under ABC analysis, the materials from group ‘A’ are purchase in lower quantities as much as possible. With this, the effort to reduce the delivery period is also made. These in turn help to reduce the investment in material.

b. Optimization of Inventory management function: Each class of the inventory gets management attention as per its value and accordingly, manpower is allocated and expenses are incurred to manage it. It ensures that most important items are regularly monitored and closely observed whereas such efforts are expended with for the less important items.

c. Control on high value material: under ABC analysis, strict control can be exercised to the materials in group ‘A’ that have higher value.

Disadvantage of ABC analysis

a) No Proper classification of material: ABC analysis will not be effective if the material is not classified into the groups properly.

b) Not suitable if materials are of same value: It is not suitable for the organization where the costs of materials do not vary significantly.

c) No scientific base: There is no any scientific base for the classification of material under ABC analysis.

Finally, you reached at the end of the post. Hope you are satisfied with BCOE 143 Solved Assignment 2022 – 23. Visit official website of IGNOU to download IGNOU BCOM assignment papers.

***