ECO 10 Solved Assignment 2022 – 23

IGNOU B.Com Free Solved Assignment 2022 – 23

Elements of Costing ECO 10 Solved Assignment 2022 – 23

COURSE TITLE: ELEMENTS OF COSTING

ASSIGNMENT CODE: ECO-10/TMA/2022-23

COVERAGE: ALL BLOCKS

Maximum Marks: 100

In this post, you will get ECO 10 Solved Assignment 2022 – 23. For Free B.Com IGNOU Solved Assignments 2022 – 23, you can visit our website regularly or you can download our mobile application. We will try to provide IGNOU Solved Assignments 2022 – 23 for BA, MA, MCOM, BBA and MBA also.

Attempt all the questions.

1. What is cost accounting? What are the major advantages of Cost Accounting to a manufacturing concern? (10+10)

Ans: Introduction to Cost Accounting

Cost: The term ‘cost’ has to be studied in relation to its purpose and conditions. As per the definition by the Chartered Institute of Management Accountants (C.I.M.A.), London ‘cost’ is the amount of actual expenditure incurred on a given thing.

Costing: The C.I.M.A., London has defined costing as the ascertainment of costs. “It refers to the techniques and processes of ascertaining costs and studies the principles and rules concerning the determination of cost of products and services”.

Cost Accounting: It is the method of accounting for cost. The process of recording and accounting for all the elements of cost is called cost accounting. I.C.M.A. has defined cost accounting as follows: “The process of accounting for cost from the point at which expenditure is incurred or committed to the establishment of its ultimate relationship with cost centers and cost units. In its widest usage it embraces the preparation of statistical data, the application of cost control methods and the ascertainment of the profitability of activities carried out or planned”.

Cost Accountancy: The term ‘Cost Accountancy’ includes Costing and Cost accounting. Its purposes are Cost-control and Profitability – ascertainment. It serves as an essential tool of the management for decision-making.

I.C.M.A., has defined cost accountancy as follows: “The application of costing and cost accounting principles, methods and techniques to the science, art and practice of cost control and the ascertainment of profitability. It includes the presentation of information derived there from for the purpose of managerial decision making”.

Nature of Cost Accounting: The nature of cost accounting can be brought out under the following headings:

1. Cost accounting is a branch of knowledge: Though considered as a branch of financial accounts, cost accounting is one of the important branch of knowledge, i.e., a discipline by itself. It is an organised body of knowledge consisting of its own principles, concepts and conventions. These principles and rules vary from industry to industry.

2. Cost accounting is a science: Cost accounting is a science as it is a body of systematic knowledge relating to not only cost accounting but relating to a wide variety of subjects such as law, office practice and procedure, data processing, production and material control, etc. It is necessary for a cost accountant to have intimate knowledge of all these field of study in order to carry on his day-to-day activities. But it is to be admitted that it is not a perfect science as in the case of natural science.

3. Cost accounting is an art: Cost accounting is an art in the sense it requires the ability and skill on the part of cost accountant in applying the principles, methods and techniques of cost accountancy to various management problems. These problems include the ascertainment of cost, control of costs, ascertainment of profitability, etc.

4. Cost accounting is a profession: In recent years cost accounting has become one of the important professions which have become more challenging. This view is evident from two facts. First, the setting up of various professional bodies such as the Institute of Cost accountant in India, ICMAI in USA and the institute of cost and management Accountants in UK. Such professional bodies both in developed and developing countries have increased the growing awareness of costing profession among the people. Secondly, a large number of students have enrolled in these institutes to obtain costing degrees and memberships for earning their livelihood.

Advantages of Cost Accounting (Aid to Management)

a) Helps in Decision Making: Cost accounting helps in decision making. It provides vital information necessary for decision making. For instance, cost accounting helps in deciding:

1. Whether to make a product buy a product?

2. Whether to accept or reject an export order?

3. How to utilize the scarce materials profitably?

b) Helps in fixing prices: Cost accounting helps in fixing prices. It provides detailed cost data of each product (both on the aggregate and unit basis) which enables fixation of selling price. Cost accounting provides basis information for the preparation of tenders, estimates and quotations.

c) Formulation of future plans: Cost accounting is not a post-mortem examination. It is a system of foresight. On the basis of past experience, it helps in the formulation of definite future plans in quantitative terms. Budgets are prepared and they give direction to the enterprise.

d) Avoidance of wastage: Cost accounting reveals the sources of losses or inefficiencies such as spoilage, leakage, pilferage, inadequate utilization of plant etc. By appropriate control measures, these wastages can be avoided or minimized.

e) Highlights causes: The exact cause of an increase or decrease in profit or loss can be found with the aid of cost accounting. For instance, it is possible for the management to know whether the profits have decreased due to an increase in labour cost or material cost or both.

f) Reward to efficiency: Cost accounting introduces bonus plans and incentive wage systems to suit the needs of the organization. These plans and systems reward efficient workers and improve productivity as well improve the morale of the work -force.

g) Prevention of frauds: Cost accounting envisages sound systems of inventory control, budgetary control and standard costing. Scope for manipulation and fraud is minimized.

h) Improvement in profitability: Cost accounting reveals unprofitable products and activities. Management can drop those products and eliminate unprofitable activities. The resources released from unprofitable products can be used to improve the profitability of the business.

i) Preparation of final accounts: Cost accounting provides for perpetual inventory system. It helps in the preparation of interim profit and loss account and balance sheet without physical stock verification.

j) Facilitates control: Cost accounting includes effective tools such as inventory control, budgetary control and variance analysis. By adopting them, the management can notice the deviation from the plans. Remedial action can be taken quickly.

2. What do you mean by cost? What are the different methods of costing? Distinguish between direct cost and indirect cost. (10+10)

Ans: Cost: The term ‘cost’ has to be studied in relation to its purpose and conditions. As per the definition by the Chartered Institute of Management Accountants (C.I.M.A.), London ‘cost’ is the amount of actual expenditure incurred on a given thing.

Methods of Costing

The methods of costing are as follows:

1) Job Costing: The job costing methods are applicable where the unit of manufacture is one and complete in itself. They include printers, job foundries, tool manufactures, and contractors, etc.

2) Contract Costing: This method if applied in undertakings erecting buildings or carrying out constructional works, e.g., House buildings, ship building, Civil Engineering contracts. Here the cost unit is one and completed in itself. The cost unit is a contract which may continue for over more than a year. It is also known as the Terminal Costing, since the works are to be completed within a specified period as per terms of contract or agreement executed by the contractor and contractee.

3) Batch Costing: In this method, a batch of similar or identical products is treated as a job. Here the unit of cost is a batch of group of products, costs are collected and analyzed according to batch numbers and the costs are ascertained batch wise. This method is applied in pharmaceutical industries where medicines or injections are manufactures batch wise or in general engineering factories producing components in convenient batches.

4) Process Costing: Process costing method is applicable to those industries manufacturing a number of units of output requiring processing. Here an article has to undergo two or more processes for reaching the stage of finished goods and succeeding process till completion.

5) Unit costing: This method is also known as single or output costing. The objective of this method is to ascertain the total cost as well as the cost per unit. A cost sheet is prepared taking into account the cost of material, labour and overheads, Unit costing is applicable in the case of mines, oil drilling units, cement works, brick works and units manufacturing cycles, radios, washing machines etc.

6) Operating costing: This method is followed by industries which render services. To ascertain the cost of such services, composite units like passenger kilometers and tone kilometers are used for ascertaining costs. For example, in the case of a bus company, operating costing indicates the cost of carrying a passenger per kilometer.

7) Operation costing: This is a more detailed application of process costing. It involves costing by every operation. This method is used where there is mass production of repetitive nature involving a number of operations. The main purpose of this method is to ascertain the cost of each operation.

8) Multiple Costing: It is also known as composite costing. It refers to a combination of two or more of the above methods of costing. It is adopted in industries where several parts are produced separately and assembled to a single product.

Difference between Direct Cost and Indirect Cost (10 Points of difference)

Direct costs are those which are incurred for and may be conveniently identified with a particular cost centre or cost unit. Materials used and labour employed are common examples of direct costs.

Indirect costs are those cost which are incurred for the benefit of number of cost centers or cost units and cannot be conveniently identified with a particular cost centre or cost unit. Examples of indirect cost include rent of building, management salaries, machinery depreciation etc.

Full Notes Available in Our Mobile Application For Free

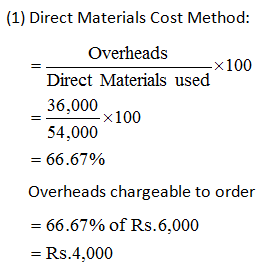

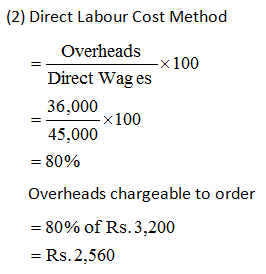

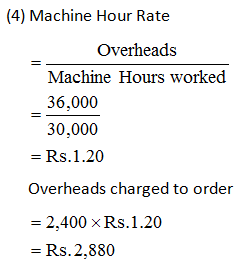

3. The production department of a factory furnishes the following information for the month of October, 2020. +

|

|

Rs. |

Hours |

|

Material used |

54,000 |

|

|

Direct Wages |

45,000 |

|

|

Overheads |

36,000 |

|

|

Labour hours worked |

|

36,000 |

|

Machine hours worked |

|

30,000 |

For an order executed by the department during October, the relevant data is as follows:

|

|

Rs. |

Hours |

|

Material used |

6,000 |

|

|

Direct Wages |

3,200 |

|

|

Labour hours worked |

|

3,200 |

|

Machine hours worked |

|

2,400 |

Calculate the overheads chargeable to the job by:

(a) Direct Materials Cost Method,

(b) Direct Labour Cost Method,

(c) Labour Hour Rate, and

(d) Machine Hour Rate.

4. What do you understand by materials control? What are the important requirements of an efficient system of material control? (10+10)

Ans: Inventory or Store Control: Inventory control means to monitor the stock of goods used for production, distribution and captive (self) consumption. For a specific time period, stocks of goods are placed at some particular location. Stock of goods includes raw-materials, work in progress, finished goods, packaging, spares, components, consumable items, etc. Inventory Control means maintaining the inventory at a desired level. The desired-level keeps on fluctuating as per the demand and supply of goods.

According to Gordon Carson, “Inventory control is the process whereby the investment in materials and parts carried in stocks is regulated, within pre-determined limits set in accordance with the inventory policy established by the management.”

Simply “Inventory control is a method to identify those stocks of goods, which can be used for the production of finished goods. It shall be supported by a schedule which gives details regarding; opening stock, receipt of raw materials, issue of materials, closing stock, and scrap generated.”

Objectives of store control: The following are the important objectives of store control

a) to make available the right type of raw material at the right time in order to have smooth and continuous flow of production;

b) to ensure effective utilization of material;

c) to prevent over stocking of materials and consequent locking up of working capital;

d) to procure appropriate quality of raw materials at reasonable price;

e) to prevent losses during storage of materials;

f) to supply information to the management regarding the cost of materials and the availability of stock;

Essential of store control: The following at the essentials of good system of material control.

a) There should be proper co-operation and co-ordination among the departments dealing with materials.

b) All purchases must be centralized and must be made through an expert purchase manager.

c) All items in the stores should be classified with codes.

d) Receiving and inspection procedure should be chalked out.

e) Ideal storage and preservation facilities will have to be provided.

f) Stores control measures like ABC analysis, perpetual inventory system, stock verification should be introduced.

g) There should be an efficient system of internal audit and internal check.

h) Maximum level, minimum level and re-order level of stock should be fixed to avoid over-stocking or shortage of materials.

i) Appropriate records should be maintained to control issues and utilization of stores in production.

j) There should be a system of regular reporting to management regarding materials purchases, storage and utilization.

5. Write short notes on the following: (4×5)

(a) Methods of absorption.

Ans: The most important step in the overhead accounting is ‘Absorption’ of overheads. CIMA defines absorption as, ‘the process of absorbing all overhead costs allocated or apportioned over a particular cost center or production department by the units produced.’ In simple words, absorption means charging equitable share of overhead expenses to the products. As the overhead expenses are indirect expenses, the absorption is to be made on some suitable basis. The basis is the ‘absorption rate’ which is calculated by dividing the overhead expenses by the base selected. A base selected may be any one of the basis given below. The formula used for deciding the rate is as follows,

Overhead Absorption Rate = Overhead Expenses/ Units of the base selected.

The methods used for absorption are as follows:

a. Direct Material Cost: Under this method, the overheads are absorbed on the basis of percentage of direct material cost. The following formula is used for working out the overhead absorption percentage: Budgeted or Actual Overhead Cost/ Direct Material Cost X 100

b. Direct Labor Cost Method: This method is used in those organizations where labor is a dominant factor in the total cost. Under this method, the following formula is used for calculating the overhead absorption rate: Budgeted or Actual Overheads/ Direct Labor Cost X 100

c. Prime Cost Method: This method is an improvement over the first two methods. Under this method, the Prime Cost is taken as the base for calculating the percentage of absorption of overheads by using the following formula: Budgeted or Actual Overheads/ Prime Cost X 100

d. Production Unit Method: This method is used when all production units are similar to each other in all respects. Total overhead expenses are divided by total production units for computing the rate per unit of overheads and overheads are absorbed in the product units. If a firm produce more than one products and if they are not uniform to each other, equivalent units are calculated to find out the rate of overheads per unit. The formula of absorption of overheads is as follows: Overhead absorption rate = Budgeted or Actual Overheads/Production Units

e. Direct Labor Hour Method: Under this method, the rate of absorption is calculated by dividing the overhead expenses by the direct labor hours. The formula is as follows. Budgeted or Actual Overhead Expenses/Direct Labor Hours

f. Machine Hour Rate: Where machines are more dominant than labor, machine hour rate method is used. CIMA defines machine hour rate as ‘actual or predetermined rate of cost apportionment or overhead absorption, which is calculated by dividing the cost to be appropriated or absorbed by a number of hours for which a machine or machines are operated or expected to be operated’. In other words, machine hour rate is the cost of operating a machine on per hour basis. The formula for calculating the machine hour rate is, Budgeted or Actual Overhead Expenses/ Machine Hours

g. Selling Price Method: In this method, selling price of the products is used as a basis for absorbing the overheads. The logic used is that if the selling price is high, the product should bear higher overhead cost. Ratio of selling price is worked out and the overheads are absorbed.

(b) Rowan premium plan.

Ans: Rowan System or Rowan Plan: The scheme was introduced in 1901 by David Rowan of Glasgow, England. The wages are calculated on the basis of hours worked whereas the ‘bonus is that proportion of the wages of time taken which the time saved bears to the standard time allowed’. Total wages under this scheme is calculated with the help of the following formula:

Earnings = Time taken x Rate per hour + Time saved / Standard time (Time taken x Rate per hour)

The main principles/features of Rowan plan are:

a) Time rate is guaranteed and the worker gets the guaranteed irrespective of whether he completes the job within the time also takes more time to do it.

b) Standard time and standard work are fixed for the job or operation in advance;

c) The workers producing more than the standard, or the workers completing the work in less than the standard time fixed, get bonus in addition to the ordinary time wage.

d) Bonus is based on that proportion of the time wages which the time saved bears to the standard time.

e) Workers who fail to reach the prescribed standard get the time wages.

f) Labour cost per unit of output decreases. The employer also shares the benefit of efficiency which induced him to improve the method and equipment.

g) Wages per hour increases but in the same proportion as the output.

The advantages and disadvantages of Rowan plan are as follows:

Advantages

(i) The plan assures a minimum hourly rate.

(ii) The quality of output is protected since the bonus declines after the worker has reached a given level of efficiency.

(iii) Labour cost per unit and fixed overhead cost per unit are reduced with increase in production.

Disadvantages

(i) The plan is not easily followed by most of the workers.

(ii) Efficiency beyond certain point is not rewarded. It fails to distinguish between a very efficient worker and a worker with a little more than average efficiency.

(iii) Since the employer gets a share of the wages of the time saved, the workers do not get the full benefit of their efforts.

(c) Overheads.

Ans: Aggregate of all expenses relating to indirect material cost, indirect labour cost and indirect expenses is known as Overhead. Accordingly, all expenses other than direct material cost, direct wages and direct expenses are referred to as overhead.

According to Wheldon, Overhead may be defined as “the cost of indirect material, indirect labour and such other expenses including services as cannot conveniently be charged to a specific unit.”

Blocker and WeItmer define overhead as follows: “Overhead costs are operating cost of a business enterprise which cannot be traced directly to a particular unit of output. Further such costs are invisible or unaccountable.”

Classification of overheads is the process of grouping of costs based on the features and objectives of the business organization. Classification is made according to following basis:

a) Classification according to Elements:According to this classification overhead are divided according to their elements. The classification is done as per the following details.

1. Indirect Materials

2. Indirect Labour

3. Indirect Expense

b) Functional Classification:Overheads can also be classified according to their functions. This classification is done as given below.

1. Manufacturing Overheads

2. Administrative Overheads

3. Selling and Distribution Overheads

4. Research and Development Overheads

c) Classification according to Behavior:According to this classification, overheads are classified as fixed, variable and semi-variable. These concepts are discussed below.

1. Fixed Overheads

2. Variable Overheads

3. Semi-variable Overheads

(d) Control Accounts.

Ans: Buy Full Assignment @ Rs. 25

Visit Official Webiste for Assignment Question Papers

***